Transition Residential Contractor to Commercial Projects

Shifting from residential to commercial contracting is defined by a fundamental change in how your business operates, not just the size of the jobs you take on. The residential to commercial transition requires new bonding capacity, upgraded insurance, different cash flow management, and a formal approach to bidding that most residential contractors have never needed before. Commercial payment terms extend to 30–60 days compared to the near-immediate terms in residential work, and commercial projects demand 3–4 times more working capital to bridge those gaps. This guide gives you the exact framework to make that pivot without putting your existing business at risk.

What are the key differences between residential and commercial contracting?

Commercial contracting is a different business model, not just a bigger version of residential work. The gap shows up in every area: bidding, compliance, client relationships, and cash flow.

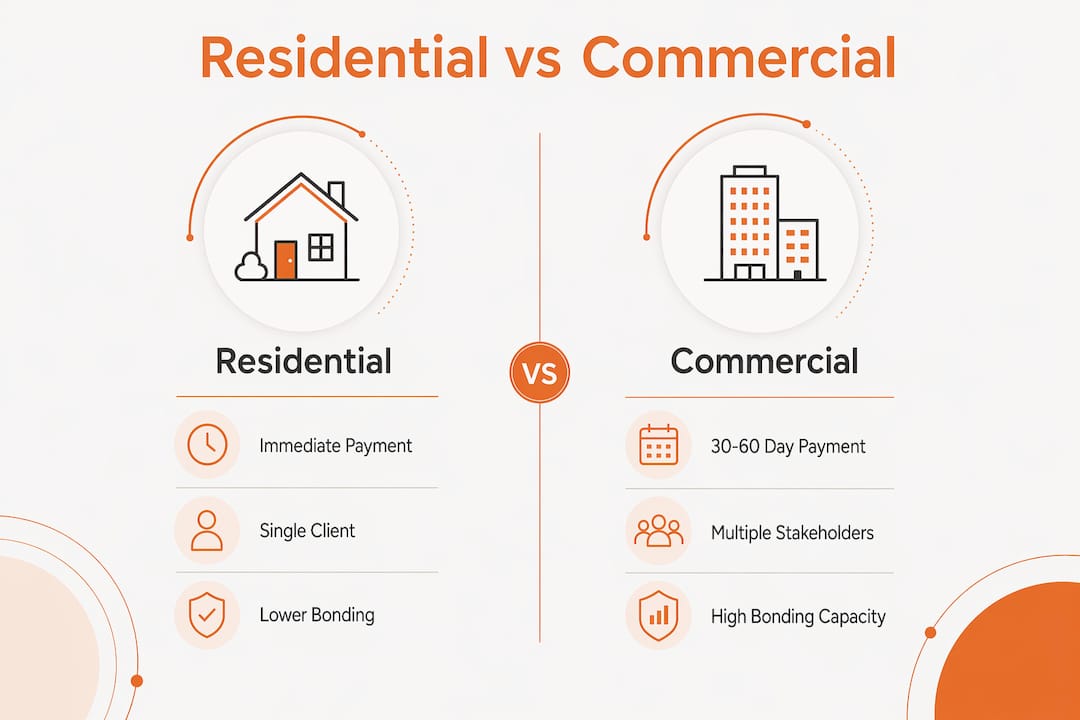

Project scale and complexity are the most visible differences. A residential job typically involves one client, one decision-maker, and a handful of subcontractors. A commercial project can involve 15–30 or more subcontractors, multiple stakeholders, and formal procurement processes with strict documentation requirements.

Client expectations shift from personal to professional. Residential clients hire you based on referrals and personal trust. Commercial clients prioritize predictable schedules, safety records, and proof of compliance. You are no longer selling yourself. You are selling your company’s systems and track record.

Here is a direct comparison of the two models:

| Category | Residential | Commercial |

|---|---|---|

| Payment terms | Immediate to 7 days | 30–60 days |

| Bonding requirement | Rarely required | Often $10M–$15M capacity |

| Insurance liability | Standard coverage | Often $5M+ liability |

| Subcontractors managed | 2–5 per project | 15–30+ per project |

| Client relationship | Personal, homeowner-driven | B2B, multi-stakeholder |

| Compliance burden | Moderate | High (OSHA, ADA, fire codes) |

The compliance gap is where residential contractors most often get surprised. Commercial projects require pre-job documentation including risk assessments, method statements, and construction phase plans. These are not optional. Missing them can disqualify your bid or expose you to liability on site.

Key operational differences to prepare for:

- Bidding process: Commercial bids are formal, competitive, and specification-driven. Bid exclusions must be explicit and detailed.

- Contract complexity: Commercial contracts reference state-specific statutes that can override standard terms. Residential contracts rarely carry that risk.

- Scheduling demands: Commercial general contractors hold subcontractors to tight milestones. Delays trigger financial penalties.

- Regulatory compliance: OSHA standards, ADA requirements, and local fire codes apply at a level of scrutiny that residential work rarely faces.

What financial preparations are essential before pivoting to commercial work?

Financial readiness is the single biggest predictor of success when you pivot to commercial projects. Most residential contractors underestimate how much capital the shift requires.

A $10 million residential contractor typically operates with $300,000–$400,000 in available cash. A commercial contractor at the same revenue level needs $800,000–$1.2 million to manage longer payment cycles without straining operations. That gap is not a minor adjustment. It requires deliberate planning before you take on your first commercial job.

Key financial controls to put in place before you start:

- Separate P&Ls for each division. Running residential and commercial revenue through the same books distorts profitability. Shared costs like equipment, vehicles, and office overhead must be allocated fairly from day one.

- Build bonding capacity early. Pursuing a $5 million commercial project typically requires $10M–$15M bonding capacity. Your surety relationship and financial statements need to support that before you bid. Read more about bonding and business growth to understand what lenders and sureties look for.

- Cap commercial revenue at 25% initially. Keep commercial income below 25% of total revenue until your financial controls and cash flow management are mature. This protects your residential base if a commercial project runs long or slow-pays.

- Build a contingency reserve. Standard commercial practice calls for contingency allowances of 3–5% on fully issued documents and 10–15% on design-build projects. Budget for this before you price a single job.

- Manage payment cycle exposure. Commercial payment terms mean you may carry 60 days of labor and material costs before receiving payment. A line of credit sized for that exposure is not optional.

Pro Tip: Starting commercial bidding when residential work slows is the fastest way to underprice and collapse your margins. Enter commercial work from a position of financial strength, not desperation. Financial stability before expanding is the rule, not the exception.

How should contractors approach bidding and contract negotiation in commercial construction?

Commercial bidding rewards precision. Thin margins mean a single estimating error can turn a profitable job into a loss. The construction estimating process for commercial work is fundamentally different from residential cost-plus or allowance-based pricing.

Follow these steps to build a competitive and protected commercial bid:

- Master commercial blueprint reading and specifications. Commercial drawings include architectural, structural, mechanical, electrical, and plumbing sets. You must read all of them before pricing. Missing a spec section is not a defense against a scope dispute.

- Write explicit bid exclusions. Every item not included in your price must be listed in writing. Profit vulnerability often lies in bid exclusions. Owners and GCs will fill gaps at your expense if you leave them open.

- Price indirect costs accurately. Commercial projects carry administrative overhead, compliance costs, and coordination time that residential work does not. Failing to price these in is the most common reason residential contractors lose money on their first commercial jobs.

- Review every contract clause before signing. Contract negotiation mistakes stem from ambiguous pricing terms, form misuse, and failure to address state-specific statutory overrides. Review indemnification clauses, payment trigger language, and lien rights in every state where you work.

- Negotiate scope, not just price. The best commercial contractors negotiate what is included before they negotiate the number. Clarifying scope upfront prevents change order disputes that erode margins after the contract is signed.

Pro Tip: Review your estimating best practices annually. Commercial bid environments shift with material costs and labor markets. A pricing model built in one year can be dangerously outdated the next.

What operational changes are required for commercial project management?

Commercial project management requires a different crew structure, a heavier administrative load, and a compliance posture that most residential operations are not built for. These are not incremental upgrades. They are structural changes.

Misapplying residential pricing logic in commercial sectors underestimates administrative and compliance overhead. That gap shows up in profitability and caps your growth ceiling faster than any other factor.

Crew and equipment scaling must happen before you win the work, not after. Commercial projects require crews experienced with commercial-grade equipment, formal safety programs, and multi-trade coordination. Sending a residential crew to a commercial site without preparation creates safety exposure and schedule risk.

Insurance upgrades are non-negotiable. Commercial projects require liability coverage of $5 million or more. Your current residential policy almost certainly does not meet that threshold. Confirm your coverage limits before you submit a single commercial bid.

Operational requirements by category:

| Area | What changes |

|---|---|

| Safety compliance | OSHA 30 certification, written safety programs, incident reporting |

| Documentation | Risk assessments, method statements, construction phase plans |

| Scheduling | Milestone-based schedules with float analysis and look-ahead planning |

| Subcontractor management | Formal scopes of work, lien waivers, insurance certificates |

| Client communication | Written RFIs, submittals, and change order logs replace phone calls |

The administrative burden alone surprises most contractors making this shift. Pre-job documentation requirements in commercial contracting include risk assessments, method statements, COSHH assessments, and construction phase plans. Building systems to produce and track these documents is a prerequisite, not an afterthought. For guidance on bonding requirements for small contractors, the process starts well before your first commercial bid.

Key Takeaways

Successfully making the residential to commercial transition requires financial controls, bonding capacity, precise estimating, and operational systems that most residential businesses must build from scratch.

| Point | Details |

|---|---|

| Working capital gap | Commercial work requires 3–4 times more working capital than residential to cover 30–60 day payment cycles. |

| Bonding before bidding | Secure $10M–$15M bonding capacity before pursuing $5M commercial projects. |

| Separate your financials | Run distinct P&Ls for residential and commercial divisions from day one to protect profitability. |

| Bid exclusions protect margins | List every item not included in your price explicitly to prevent costly scope disputes. |

| Cap commercial revenue early | Keep commercial work below 25% of total revenue until your cash flow controls are proven. |

What I’ve learned after watching contractors make this shift

The contractors who fail at commercial work almost always make the same mistake. They treat it as bigger residential work. They bring the same crew, the same pricing habits, and the same client communication style. Then they wonder why the job bleeds money.

Commercial success rewards structure and risk management, not speed or hustle. I have seen mid-sized firms scale from $5 million to $50 million in revenue, and the ones that made it did not sprint into commercial work. They built the infrastructure first. Separate financials. Bonding relationships. Formal estimating systems. Safety programs with documentation. Then they bid.

The hybrid model works best for most contractors making this pivot. Maintain a steady residential base that covers overhead, and target 2–3 commercial accounts that represent 20–30% of revenue. That structure gives you margin stability and scheduling flexibility while you build commercial experience without betting the whole business on it.

One more thing that rarely gets said: your first commercial contract negotiation will feel like a different language. State-specific statutes can override standard contract terms in ways that are not obvious until a dispute arises. Get a construction attorney to review your first few commercial contracts. That cost is far smaller than the cost of a payment dispute on a $2 million job.

The contractors who build durable commercial businesses do it incrementally. They do not abandon residential work. They use it as a foundation while they develop the systems, relationships, and financial controls that commercial clients require.

— Rowena

How Rconstructionsolutions supports your commercial transition

Rconstructionsolutions has spent over 30 years working directly with contractors navigating exactly this kind of shift. The work is not generic consulting. It is hands-on guidance built around your specific numbers, your crew, and your market.

Whether you need help structuring your financials for bonding, building a commercial estimating process, or reviewing your first commercial contract, the construction consulting services at Rconstructionsolutions are built for that work. Contractors also use The Sandbox for practical estimating templates and bidding tools designed specifically for the commercial environment. If you are ready to build a commercial division that does not put your residential business at risk, Rconstructionsolutions has the framework to get you there.

FAQ

What is the biggest financial risk when transitioning to commercial work?

The biggest risk is insufficient working capital. Commercial projects require 3–4 times more cash reserves than residential work due to 30–60 day payment cycles.

How much bonding capacity do I need to bid commercial projects?

Pursuing a $5 million commercial project typically requires $10M–$15M in bonding capacity. Build your surety relationship and financial statements before you bid.

Should I stop residential work when I go commercial?

No. A hybrid model with 70–80% residential and 20–30% commercial revenue provides the margin stability and cash flow needed while you build commercial experience.

What insurance coverage does commercial work require?

Commercial projects commonly require general liability coverage of $5 million or more. Confirm your policy limits before submitting any commercial bid.

How long does the residential to commercial transition take?

A realistic timeline is 6–12 months to put the financial controls, bonding, insurance, and operational systems in place before actively pursuing commercial contracts.